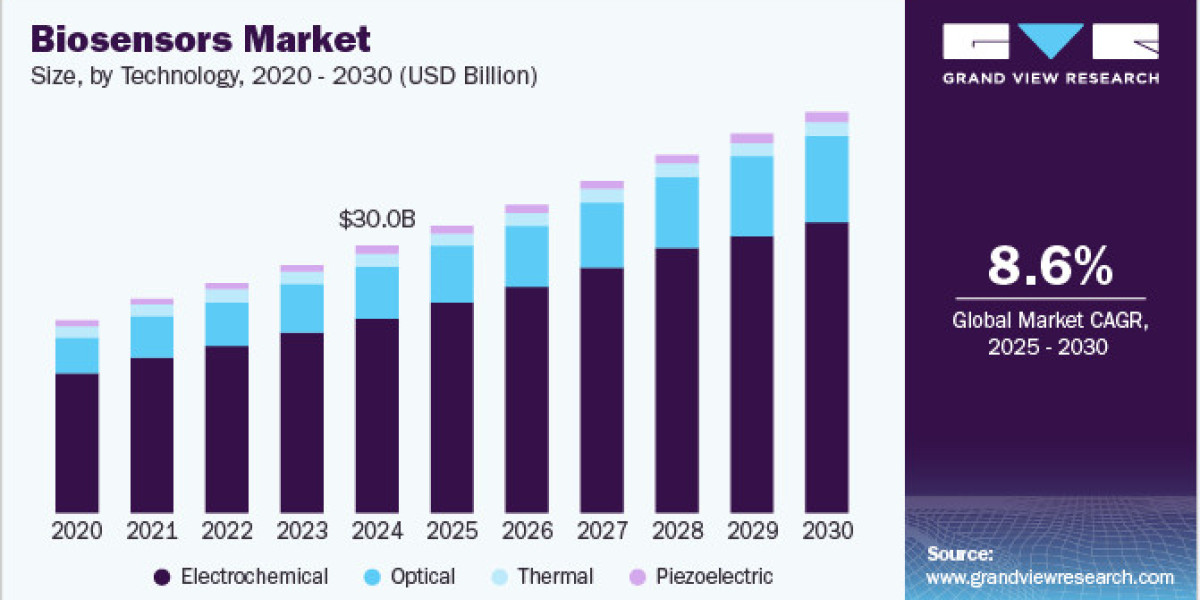

The global biosensors market was valued at USD 30.0 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 8.6% from 2025 to 2030. This growth is fueled by the broad range of medical applications, the rising prevalence of diabetes, increasing demand for compact diagnostic devices, and rapid technological advancements. Accurate and early disease diagnosis plays a crucial role in improving patient outcomes and survival rates. In recent years, there has been a surge in demand for disposable, user-friendly, cost-effective devices that offer rapid results. Additionally, the COVID-19 pandemic positively influenced the medical device sector, as various methods were employed to detect early symptoms of the virus.

The biosensors market is poised for significant growth, driven by continuous technological innovations and strategic initiatives from leading industry players. For example, in January 2023, Intricon, a developer and manufacturer specializing in medical devices with smart miniaturized electronics, took a major step forward by launching a Biosensors Center of Excellence (CoE). This strategic initiative underscores Intricon’s dedication to integrating its expertise into a vertically aligned business unit focused on delivering biosensor solutions to the medical field. The combination of innovation and targeted strategy is accelerating positive developments across the biosensors industry.

Technology Insights

By technology, the market is segmented into piezoelectric, electrochemical, thermal, and optical categories. In 2024, the electrochemical segment accounted for the largest market share at 71.7% and is anticipated to grow at the fastest CAGR of 8.7% from 2025 to 2030. The dominance of electrochemical biosensors is attributed to their widespread application in biochemical and biological analyses. Their advantages—such as low detection limits, a broad linear response range, excellent stability, and high repeatability—make them preferable over piezoelectric, thermal, and optical alternatives, leading to greater market adoption.

Application Insights

The market, based on application, is divided into bioreactor, medical, agriculture, environmental, food toxicity, and others. In 2024, the medical segment led the market, capturing 66.8% of total revenue. Biosensors play a pivotal role in medical diagnostics, being used for cholesterol tests, blood glucose monitoring, drug discovery, pregnancy testing, blood gas analysis, and detecting infectious diseases. They are essential tools for diagnosing and monitoring a wide spectrum of conditions, including diabetes and cancer. Meanwhile, the agriculture segment is expected to register the fastest CAGR of 9.8% from 2025 to 2030.

Get a preview of the latest developments in the Global Biosensors Market! Download your FREE sample PDF today and explore key data and trends

End-User Insights

End-users in the market include research laboratories, the food industry, home healthcare diagnostics, security point-of-care (PoC) testing, and bio-defense. In 2024, PoC testing led the market with a 47.9% revenue share. The segment’s growth is propelled by technological advancements that have introduced ultra-sensitive, printable biosensors for PoC applications, enabling the detection and monitoring of organic fluids such as urine, saliva, blood, and sweat.

Regional Insights

In 2024, North America held the largest market share, accounting for over 40.2% of total revenue. This dominance is attributed to the presence of key market players and a high incidence of target diseases in the region. Looking ahead, market growth is expected to be supported by ongoing technological developments—such as miniaturized diagnostic devices that enhance Electronic Medical Records (EMR) integration and deliver precise, rapid results. Moreover, U.S. environmental regulations, including the Clean Air Act, Clean Water Act, and National Environmental Policy Act, are anticipated to create further growth opportunities within the region.

Key Companies in the Biosensors Market

The following leading companies collectively hold the largest market share and play a pivotal role in shaping industry trends. Their financials, strategic roadmaps, and product portfolios contribute to mapping the global supply chain:

- Abbott Laboratories

- Medtronic

- Biosensors International Group

- Pinnacle Technology, Inc.

- Dupont

- Sensirion AG

- Thermo Fisher Scientific, Inc.

- F. Hoffmann-La Roche AG

- Siemens Healthineers

- Zimmer & Peacock AS

- Metrohm AG

- DexCom, Inc.

- Universal Biosensors, Inc.

- Johnson & Johnson Services, Inc.

- Nix Biosensors

- Cyrcadia Health

- Lifescan

Gather more insights about the market drivers, restrains and growth of the Biosensors Market